How Do Real Estate Agents Get Paid? A Simple, Honest Breakdown

How does a real estate agent actually get paid — and what does a commission check really look like after everything comes out?

Most people getting into real estate understand the concept: you help someone buy or sell a home, a commission is paid, and some of it comes to you. But the gap between that understanding and what actually happens is significant. And if you don't understand the mechanics before your first closing, the number on your check is going to surprise you.

Here's how it actually works.

The Money Flows Through the Transaction — Not to You Directly

When a home sale closes in Florida, the commission doesn't come straight from the seller to you. It flows through the transaction itself — typically disbursed by the title company at closing according to the agreed commission distribution.

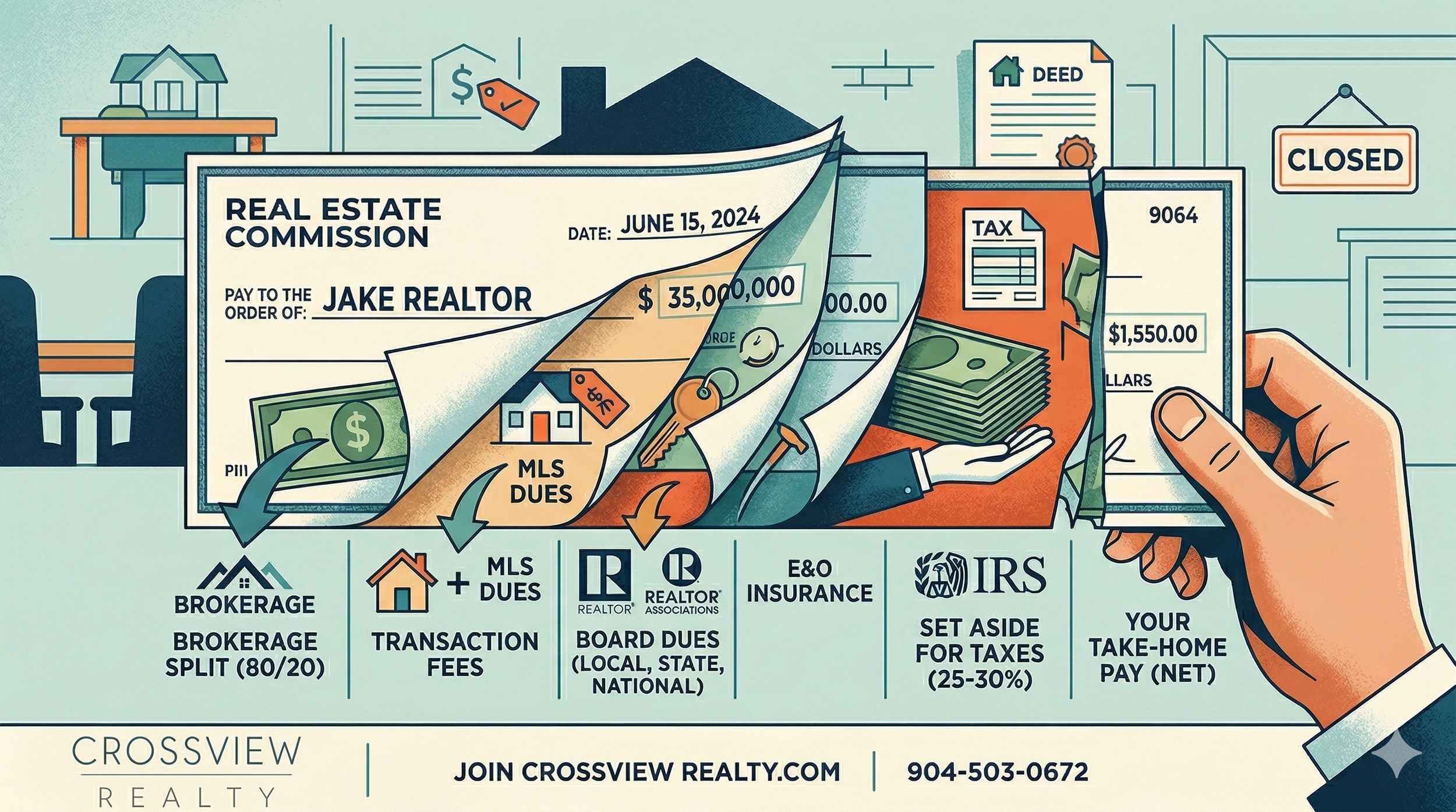

Your brokerage receives its portion. From there, your share is paid out according to your agreement with the brokerage — your split. If you're on an 80/20 split, the brokerage keeps 20% and you receive 80% of the commission allocated to your side of the transaction.

That number — your percentage of the commission — is your Gross Commission Income, or GCI. It's the starting point. It's not what you take home.

For a deeper look at how splits, caps, and fee structures compare across different brokerage models, we covered that in detail in our post on splits vs. caps vs. fees.

What Comes Out Before You See the Money

Your GCI gets reduced by expenses — some taken directly at closing, others billed separately throughout the year. Here's what new agents in Jacksonville and across Northeast Florida are typically dealing with:

Brokerage fees and split. Already accounted for above, but worth naming clearly. This is the biggest single reduction from your gross.

Transaction fees. Some brokerages charge a flat per-transaction fee on top of the split. Know what yours is before you close your first deal.

MLS dues. Access to the Multiple Listing Service in Florida isn't free. Annual dues vary by association but are a real cost of doing business.

Board dues. If you're a member of a Realtor association — which most agents are — you'll pay annual dues at the local, state, and national levels.

E&O insurance. Errors and omissions insurance protects you if a client ever claims a mistake caused them financial harm. Many brokerages include this in their fees; others charge it separately.

Marketing and business expenses. Professional photos, business cards, signage, lockboxes, mileage — it adds up. The agents who don't account for this upfront are the ones who feel like they're barely breaking even on their first few closings.

After all of that, what remains is your net. And that's before taxes.

You Are Now a Business Owner. Taxes Don't Happen Automatically.

This is the part that catches more new agents off guard than anything else.

The moment you hang your license at a brokerage, you are an independent contractor — a 1099 worker, not a W-2 employee. Nobody is withholding taxes from your commission checks. No Social Security. No Medicare. No federal or state income tax.

That responsibility falls entirely on you.

A reliable rule of thumb: set aside 25–30% of every commission check the moment it hits your account. Move it to a separate account. Don't touch it. That money belongs to the IRS. As a self-employed agent, you'll be responsible for quarterly estimated tax payments — typically due in April, June, September, and January.

The upside? You can deduct legitimate business expenses — mileage, marketing, dues, home office use, and more. That's why keeping clean records from day one matters.

Once the money is in your hands and taxes are accounted for, the question of what to do with it is just as important as understanding how you got it. We covered exactly that in our post on what to do when you get a commission check in real estate.

A Simple Example to Make It Real

Say you help sell a $350,000 home in Jacksonville or St. Johns County. The buyer agent commission negotiated is 2.5%, so your side of the transaction generates $8,750.

After an 80/20 split with your brokerage, you receive $7,000 in GCI.

Subtract a transaction fee, your proportional share of annual dues and insurance, and set aside 25–30% for taxes — and your actual take-home on that closing might land somewhere around $4,500 to $5,000, depending on your specific costs.

That's not discouraging. It's clarifying. A $350,000 home is a very manageable first sale in this market — and that's a real check. But understanding the math helps you build a business around reality, not assumptions.

How CrossView Realty Approaches This

At CrossView Realty, we make sure agents understand the full financial picture before their first closing — not after. Knowing how you get paid, what comes out, and how to manage what's left is part of building a sustainable career. If you want to work somewhere that treats you like a professional from day one, reach out at joincrossviewrealty.com or call 904-503-0672.

Real estate income is real — but it works differently than anything else you've probably done. The agents who thrive financially are the ones who understood the mechanics early, planned for the expenses, and treated every commission check like a business transaction rather than a windfall.

Frequently Asked Questions

Q: How do real estate agents get paid in Florida? Agents are paid at or after closing through their brokerage, based on their agreed commission split. The commission is typically disbursed by the title company and flows to the broker first, then to the agent. Florida allows commission to be paid at the closing table, by check, or via direct deposit depending on brokerage structure.

Q: What is the difference between gross commission income and take-home pay for a real estate agent? Gross commission income is your share of the commission before any deductions. Take-home pay is what remains after your brokerage split, transaction fees, dues, insurance, business expenses, and taxes. The gap between the two is often larger than new agents expect.

Q: Do real estate agents pay taxes on commission checks? Yes — and nobody withholds it for them. Agents are 1099 independent contractors, meaning they're responsible for setting aside their own federal income tax, state tax where applicable, and self-employment tax covering Social Security and Medicare. Setting aside 25–30% of every check is a reliable starting point.

Q: What expenses do new real estate agents need to plan for in Florida? Key costs include MLS dues, Realtor board dues at the local, state, and national levels, E&O insurance, transaction fees, marketing expenses, and mileage. Many of these are deductible business expenses — which is why clean bookkeeping from the start matters.

Q: When does a real estate agent get paid after closing? In Florida, agents can be paid at the closing table, by mailed check, or by direct deposit. Timing varies by brokerage, but most modern brokerages pay within a few business days of closing once all paperwork is submitted and reviewed.